Introduction

Imagine you’re running a bakery. You have 100 loaves of bread baked yesterday at ₹10 each and 100 fresh ones today at ₹15 each. To maximize profit, you’d likely sell today’s pricier bread first. This is the essence of LIFO—a strategic accounting method that impacts profitability, taxes, and cash flow.

Inventory management isn’t just about stocking up; it’s about how you value what’s on your shelves. With rising costs in 2025, businesses face pressure to align inventory practices with economic trends. This guide dives deep into LIFO, its pros, cons, and real-world applications, tailored for entrepreneurs, students, and finance enthusiasts.

What is the LIFO Method?

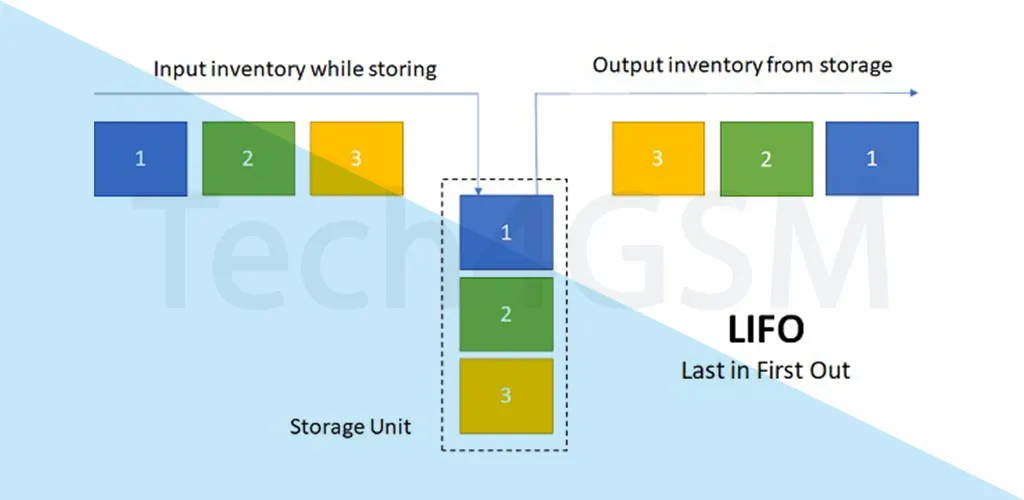

LIFO stands for Last-In-First-Out, an inventory valuation technique where the newest stock is sold first. Think of it like a stack of magazines: the latest issue sits on top and is picked first.

- Key Concept: Under LIFO, recent inventory costs are recorded as Cost of Goods Sold (COGS), while older stock remains on the balance sheet.

- Impact: During inflation, this method reduces taxable income by matching higher recent costs with current revenue.

How Does LIFO Work? A Step-by-Step Breakdown

Let’s simplify with two scenarios:

Example 1: The Grinder Business

A hardware store buys 100 grinders at ₹10 each in January 2025. In June 2025, prices rise, and they restock 100 grinders at ₹15 each.

- Sales: By year-end, 120 grinders are sold.

- COGS Calculation:

- 100 grinders (June) × ₹15 = ₹1,500

- 20 grinders (January) × ₹10 = ₹200

- Total COGS: ₹1,700

- Remaining Inventory: 80 grinders valued at ₹10 (₹800).

Tax Benefit: Higher COGS lowers taxable profit, saving money.

Example 2: Supermarket Restocking

A grocery store stacks milk cartons vertically. New stock is placed on top, so the latest cartons (bought at higher prices) sell first. This mirrors LIFO’s physical flow.

Where is LIFO Used?

- Primary Region: USA (permitted under GAAP).

- Restrictions: Banned under IFRS (used in 144+ countries, including India).

- Industries:

- Oil & Gas: Frequent price fluctuations make LIFO ideal.

- Retailers: Electronics, fashion (e.g., selling newest iPhone models first).

- Auto Dealers: High-value inventory with rising costs.

Why Isn’t LIFO Global?

- Critics argue LIFO understates profits and inflates COGS, distorting financial health. Countries like India prioritize FIFO for transparency.

When Should You Use LIFO?

Consider LIFO if:

- Prices Are Rising: Higher COGS = Lower taxable income.

- Tax Savings Are Critical: Improve cash flow for reinvestment.

- Inventory Doesn’t Expire: Older stock (e.g., machinery parts) won’t spoil.

2025 Economic Outlook: With inflation predicted to rise 4-5%, LIFO could shield businesses from profit overstatements.

LIFO Formula & Calculation

Step 1: Identify the cost of the most recent inventory.

Step 2: Multiply by the number of units sold.

Formula:

COGS=Units Sold×Cost of Newest Inventory

Case Study: Tina’s Stationery Business

- Problem: Paper costs surged from ₹200 to ₹300 per unit in 2025.

- LIFO Application:

- Sold 20 units × ₹300 (newest) = ₹6,000 COGS

- Tax Savings: ₹6,000 expense vs. ₹4,000 under FIFO.

Advantages of LIFO

- Accurate Profit Measurement:

- Matches current costs with revenue, avoiding “inventory illusion” during inflation.

- Tax Efficiency:

- Lower taxable income = More cash for growth.

- Simplified Physical Flow:

- Aligns with vertical stacking (e.g., warehouses, libraries).

Disadvantages of LIFO

- International Barriers:

- Banned under IFRS; complicates global expansion.

- Obsolete Inventory Risk:

- Older stock may become outdated (e.g., unsold tech gadgets).

- Misleading Financials:

- Understates assets on balance sheets, affecting loan approvals.

LIFO vs. FIFO: Which is Better?

| Factor | LIFO | FIFO |

|---|---|---|

| Tax Impact | Lowers taxes in inflation | Higher taxable income |

| Profit Reporting | Shows lower profits | Shows higher profits |

| Global Use | USA only | Worldwide (IFRS-compliant) |

When to Choose:

- FIFO: Stable/rising prices, perishables (e.g., food).

- LIFO: Inflationary periods, non-perishables (e.g., metals).

FAQs About LIFO

Q: Can LIFO be used in India?

A: No. India follows AS (Accounting Standards) and IFRS, prohibiting LIFO.

Q: Does LIFO affect shareholder dividends?

A: Yes. Lower reported profits may reduce dividends but improve long-term liquidity.

Q: How does LIFO impact financial ratios?

A: Lowers net income (affects P/E ratio) and understates inventory turnover.

Q: Are there alternatives to LIFO?

A: Yes! Consider FIFO, Weighted Average Cost hybrid solutions.

Conclusion: Is LIFO Right for Your Business?

If you’re a U.S.-based business facing inflation, LIFO offers tangible tax benefits. However, weigh its drawbacks—like outdated inventory and globalFor tech-driven solutions, explore tools at Tech4GSM to automate inventory tracking and maximize efficiency in 2025.

Final Takeaway: LIFO isn’t a one-size-fits-all method. Align it with your industry, location, and financial goals to make informed decisions.